Report of investment-analytical agency Era of Changes on analytical materials for the second 4 months of 2025 (statement)

![]()

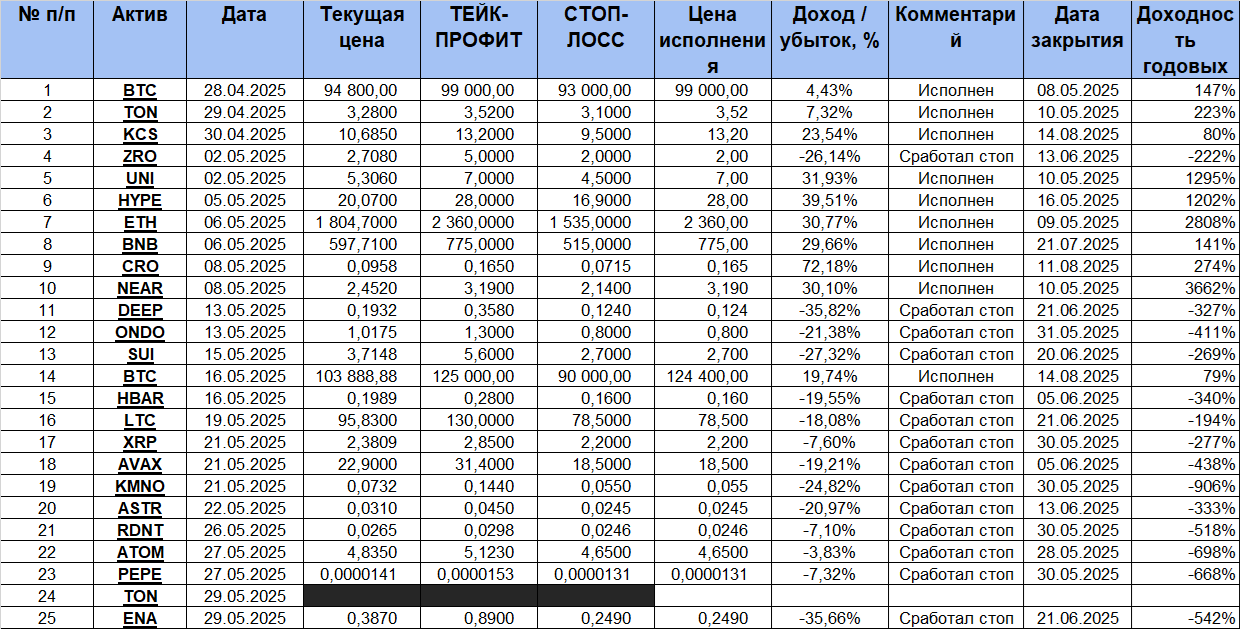

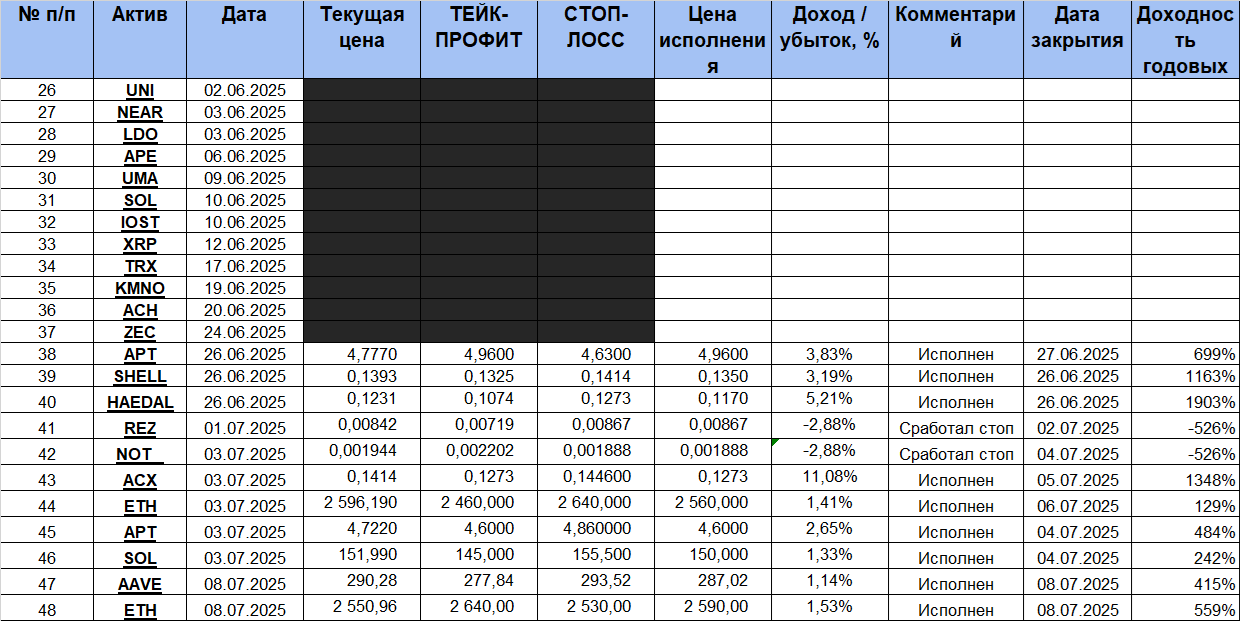

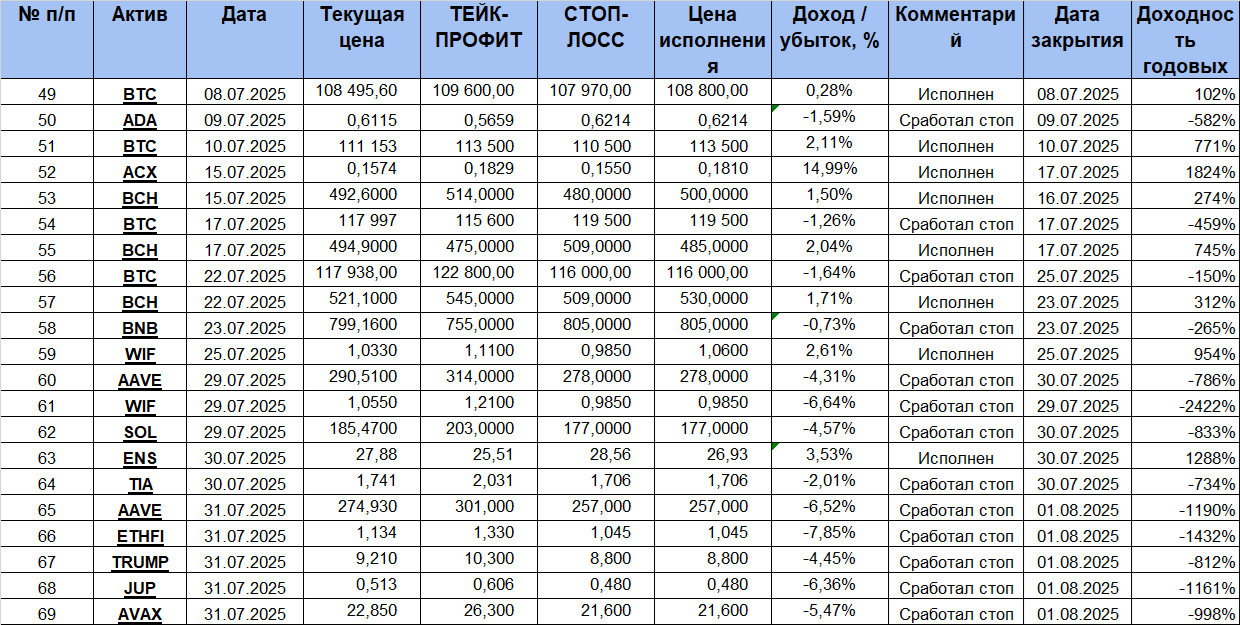

Why annualized? Because if the deal was profitable, it is important to release funds for new investments as soon as possible. If a deal made a 10% return in 5 days, it is much more efficient than in 2 months. Because that's the time the money is closed in a profitable but overextended idea.

The same applies to losing trades. If you make a lot of trades with short stop closes, like -1%, every other day, you will lose half of your portfolio in 50 trading days. But if the stop is triggered after 5 days, you will lose half of your portfolio in 250 trading days.

Why are there so many stops? Because the manager's task is to limit losses and let profits flow. Many trades closed by stops were profitable in the end. But we can't let money get stuck in these trades for long. Because that reduces the average return on investment (see first paragraph).

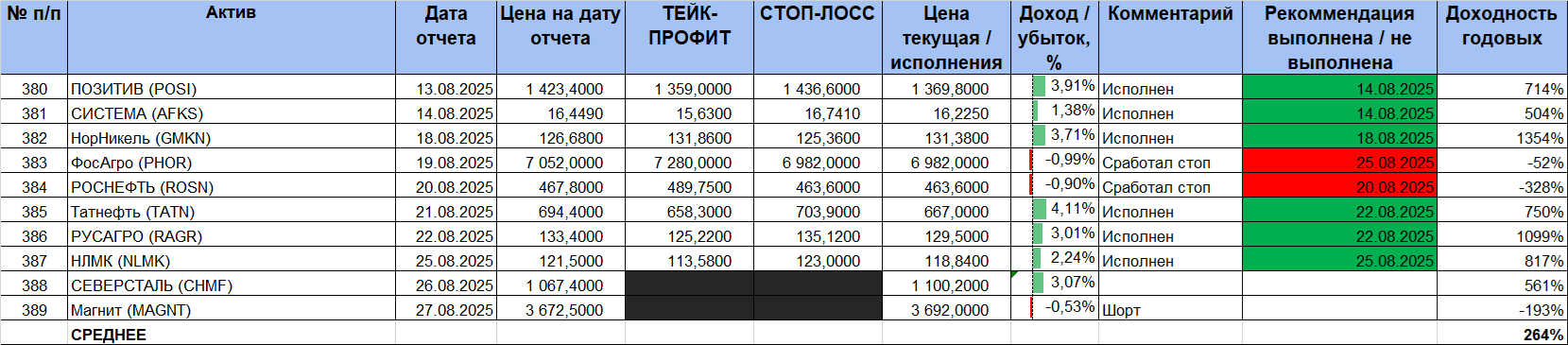

Notice the large skew in the returns of profitable trades versus unprofitable trades. That's what we're working on. The average return of profitable trades is 3.5% (580% p.a.), while the average loss of unprofitable trades is 1.1% (-176% p.a.). At the same time the number of profitable deals was higher than the number of unprofitable ones. So for the second 4 months of 2025 there were 46 (58.2%) profitable deals and 33 (41.8%) unprofitable ones.

Is it much 264% p.a. in rubles and 87% for the period? Yes it is a lot. For example, since 29.04.2025 the RGBITR index, reflecting the change in the total price value of Russian OFZ including coupon payments and excluding taxation of income in rubles has grown from 634.38 to 726.18. I.e. the purchase of Russian debt, which is comparable in risk level to opening a deposit, brought a profit of 14.5% or 44.0% per annum in rubles, i.e. 6 times less.

The Moscow Exchange Total Return Gross Index (MCFTR), which reflects the change in the total value of the prices of Russian shares included in the calculation of the Moscow Exchange Index, including dividend payments and excluding taxation of income in rubles, rose from 7357.96 to 7572.14 points during this time, i.e. showed a return of +2.9% or +9.0% p.a. in rubles, i.e. 30 times lower.

The average yield of our analytical materials on the CRIPTO market from 28.04.2025 to 27.08.2025 was 33% p.a. or 11% for the period.

This is much lower than the results for the Russian market, but still comparable to buying Russian debt (14.5% or 44.0% p.a.) and almost 4 times higher than buying Russian equities (+2.9% or +9.0% p.a.), especially since 13 deals remain outstanding and have the potential to generate substantial returns.

List of analytical materials on the Russian market

List of analytical materials on the CRIPTO market